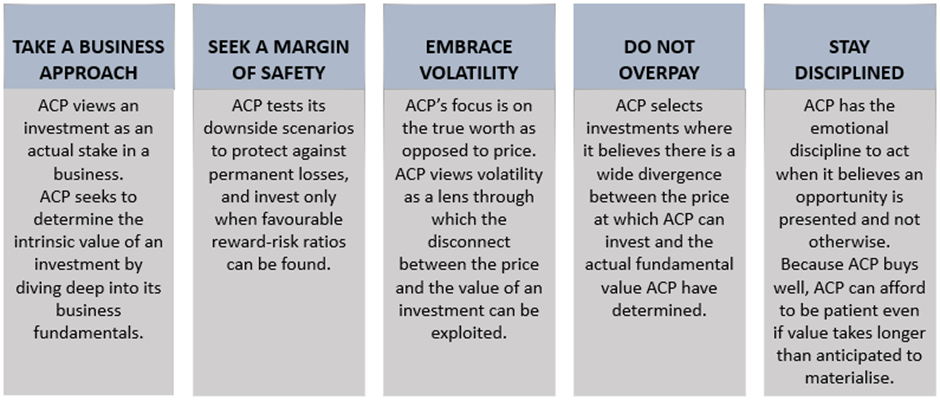

Aligned Capital Partnership knows and accepts that good ideas can come from anywhere, so the trick is to look widely

Balancing experience with reading, and by being incessantly curious, Aligned Capital Partnership believes that great ideas can be uncovered through rigorous research, intellectual honesty, constructive debate, and humility.

Aligned Capital Partnership, on behalf of the Aligned Capital Partnership Investment Trust, views itself primarily as an owner of businesses, and ideally holds its positions for a very long time with low turnover. Aligned Capital Partnership tries to think and act like successful business owners that truly take a multi-year approach in its thinking, in its portfolio management, and in the all-important temperament. Aligned Capital Partnership is not a macro investor.

An important part of the role as capital allocator of the Aligned Capital Partnership Investment Trust is being able to know when to play offense and when to play defence. This is particularly pertinent to Aligned Capital Partnership as there is limited mental capacity to understand too many investments and as a result there are only ever finite spots available in the portfolio.

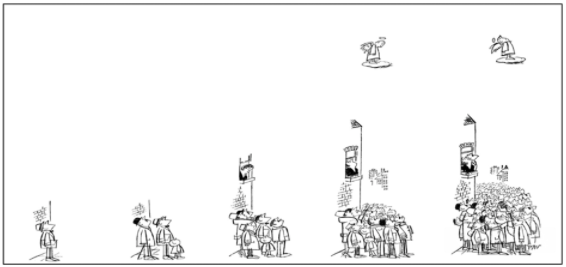

Over the years that I have been investing, I have observed that when the overall share market is weak, or when the price of an individual public listed company’s share is weak, there is a tendency for many investors to have an emotional response to the poor performance of the price, and to lose both perspective and patience. Similarly, there is also a tendency for many investors to have an emotional response to the strong performance of prices and to equally, although from the opposite standpoint, lose perspective and patience. There seems to be this fluctuation between fear and greed. I don’t think people consciously choose to invest with these emotions, many just can’t help it and that often leads to a modus operandi of “Sell before it goes to zero” or “Buy before you miss out.” Of course, there are investors who believe they are skilled enough to know when these swings in the market will occur. Such a strategy is frequently referred to as ‘market timing’. Well known economist, John Maynard Keynes had this to say of market timing: “Most of those who attempt it sell too late, buy too late, and do both too often.” I agree with Mr Keynes. I know I can’t time the market. And I don’t try to.

Before making an investment, Aligned Capital Partnership spends significant time trying to develop a good understanding of the business it is considering investing in, and the industry in which it operates. The thinking is summarised in an Investment Hypothesis. When new information about the business or the industry surfaces, the Investment Hypothesis is updated as well as the merits of an investment.

I try to manage my emotional response to price movements through conscious self-discipline.

Whenever Aligned Capital Partnership is barraged with particularly bad or good news, the Investment Hypothesis, covering investments for which such news is relevant, is re-read and then three questions are posed:

- What has really changed?

- How have the changes affected the value of the investments under consideration?

- Am I sure that I am being rational, and not overly influenced by the immediacy and the severity of the news, in my assessment of the changes?

Even though it may be tempting to flatter oneself, Aligned Capital Partnership understands it is the businesses it invests in that do almost all the heavy lifting in the wealth creation process. If Aligned Capital Partnership brings something to the investment party, it is to be more rational than other investors.

At the heart of investing is understanding why something is mis-priced. Contrary to the belief casually held by many, Aligned Capital Partnership does not think ‘it’s cheap’, ‘it’s a good company’ or ‘it’s growing rapidly’ is a sufficient reason to believe that a mispricing exists. Cheap companies can be overvalued because the businesses are deteriorating rapidly. Good companies or those experiencing rapid growth may be priced at a level that implies they are even better companies or growing faster than they are.

In his famous 1984 speech at Columbia Business School about Graham-and-Doddsville, Warren Buffett said many important things, none more profound than this: “When the price of a stock can be influenced by a ‘herd’ on Wall Street with prices set at the margin by the most emotional person, or the greediest person, or the most depressed person, it is hard to argue that the market always prices rationally. In fact, market prices are frequently nonsensical.”

I think this is profound because by accepting the idea that prices are not always rational, then they should not be the sole basis for decisions. That is the concept behind the principle of Mr. Market not being here to guide us, but to serve us.

When it comes to portfolio construction, I believe many people fail to adequately differentiate between frequency and magnitude. In other words, they conflate the frequency of being correct or incorrect with the financial impact of those outcomes.

I often hear investors say they look for a high “batting average”. What that translates into is that they are seeking a high frequency of being right. As a result, the focus is on how often they are right and not on how much money they make when they are right. Mathematically, if they make one significant error, it will offset a lot of instances where they were right. Batting average speaks to frequency.

I think the other side of a discussion involving portfolio construction should consider magnitude. That is what investors will refer to as “slugging percentage”.

These are not mutually exclusive concepts.

What drives returns to investors in the Aligned Capital Partnership Investment Trust can be expressed as the following formula:

Returns to Partnership Trust investors = Invested Capital x (Return ^ Time)

With this thinking in mind, the Aligned Capital Partnership Investment Trust portfolio is divided into the following categories:

Good Batters-

are companies where we believe we have a high probability of being able to assess what their future earnings profile looks like. These are companies that possess many of the qualities we desire, and where we have a high confidence level that they will be better businesses with higher earnings in the next five years +. Because of our ability to hold high levels of confidence in the future profile of these businesses, we consider it likely that the returns we can generate will be lower (still above what we consider our opportunity cost), but that the returns can be generated for a long period.

Fertile Grounds-

are companies where we believe we have a lower probability of being able to assess what their future earnings profile looks like than we are for Good Batters. The qualities that these businesses possess are many of those we desire, albeit fewer than, or not quite at the same levels of, those of Good Batters. Our confidence that these businesses will have higher earnings, and possibly be better businesses, in the next five years remains high, albeit lower than that we have for Good Batters. As we assign lower probabilities to Fertile Ground companies, towards some of the things we look for when making investments, than what we do to Good Batters, we consider it likely that the returns we can generate from Fertile Grounds will be higher than what we consider likely can be generated from Good Batters, but the returns generated will have a more inconsistent profile. We believe there is a reasonable probability that Fertile Grounds companies can become Good Batters.

Favourable Sluggers-

are investments we make where the returns are driven by cyclical factors, are reliant on a change in the operating environment, or that are grossly mispriced. The qualities the individual businesses in this category possess are less influential to our investment decision than is the case for Fertile Grounds and Good Batters. Our confidence level for the outlook for the drivers of the investment returns is lower than that for Fertile Grounds, but we consider it likely that the investment returns will be higher, albeit with a more inconsistent profile.

In an ideal world, near all, if not the entire, Aligned Capital Partnership Investment Trust portfolio would consist of Good Batters, acquired at attractive prices, and that never become exceedingly expensive.

Unfortunately, the world has not presented as ideal yet, so we resolve to patience in continuing to shape the portfolio, consciously aware of our own flaws, our key principles and while always weighing opportunity costs.

The mental models Aligned Capital Partnership applies to investing are those of the Hunter and the Farmer.

The Farmer aims to be a long-term, buy-and-hold investor of companies that have a high likelihood of compounding in value over years. If the investments are well looked after they will continue to grow and become more beautiful for every year they are owned. The key tasks are to water the flowers and to pull out the weeds, as famous investor Peter Lynch described it.

The Hunter looks for what Benjamin Graham famously described as being cigar butts that still have a puff or two left in them and that can be picked up for free. These are investment opportunities that are sought to be exceptionally cheap. Returns generated are irregular and there is a need for continuous replacement of investment opportunities.

Aligned Capital Partnership believes in having a somewhat balanced approach and will invest through both mental models. The degree to which I go hunting will vary significantly, depending largely on where I deem the pendulum-like swings of investment markets are between

- euphoria and depression;

- celebrating positive developments and obsessing over negatives; and

- over-priced and under-priced.

Most of the time and effort is spent on farming. Aligned Capital Partnership prefers being a ‘buy and hold’ investor in most of its holdings. Finding, researching, and getting to know companies is a slow and time-consuming process.

The Aligned Capital Partnership Investment Trust will have several investments in its portfolio. The number may vary yet is unlikely to exceed 20-25. These may include Australian and international shares, debt securities and other securities and investments deemed suitable, depending on where opportunities are perceived to be most attractive. Aligned Capital Partnership aims to generally keep its weighting in any security below 10% of the Aligned Capital Partnership Investment Trust but may exceed this level from time to time.

Most of the Aligned Capital Partnership Investment Trust’s securities are intended to either be listed on a stock exchange or can be actively traded in a market that permits independent third-party confirmation of pricing. However, some of its assets may be unlisted or have limited liquidity, hence co-investors are encouraged to take a long-term view.

Everyone has a different perspective, different objectives and different approaches. Aligned Capital Partnership’s perspective is that of an investor. That means that owning shares in a company is to have a fractional ownership of that company.

Aligned Capital Partnership makes buy and sell decisions based on the current price of the shares compared with Aligned Capital Partnership’s perceived value of the company. The objective is to invest in businesses, on behalf of the Aligned Capital Partnership Investment Trust, that can be bought at a sizeable discount to what I believe they will be worth in the future, with a reasonable margin of safety.

In my experience, the time to buy is when I think I know something others don’t know, don’t care about or prefer to ignore – when I look at something differently to what others do.

I believe that over the long run the share price of a company tends to reflect the fundamental developments involving the underlying business. This provides me with the opportunity to profit in at least one of the following three possible ways

- from free cash flow generated by the underlying business, that can be used to buy back shares or distributed as dividends, which eventually will be reflected in a higher share price;

- from an increase in the multiple that market participants are willing to pay for the underlying business as reflected in a higher share price; or

- by a narrowing of the gap between share price and underlying business value.

Speculators, by contrast, and in Aligned Capital Partnership’s opinion, buy and sell shares (and or other securities/assets) based on whether they believe those shares will next rise or fall in price. The speculators’ judgement regarding future price movements is based, not on fundamentals, but on the prediction of the behaviour of others – with a tendency to buy shares because they ‘act’ well and sell when they do not. Speculators will be seen to be obsessed with predicting – guessing – the direction of share prices.

Aligned Capital Partnership does not think anyone knows what the market will do – trying to predict is a waste of time and investing based upon prediction is, in my opinion, a speculative undertaking.

Speculation offers the prospect of instant gratification – why get rich slowly if you can get rich quickly? Moreover, speculation involves going along with the crowd, not against it. There is comfort in consensus – those in the majority gain confidence from their very number.

It is hard not to be drawn towards the crowd.

In my opinion, many financial-market participants, knowingly or unknowingly, are speculators and therefore may not even realise that they are playing a ‘greater fools’ game’.

There is great allure to treating share prices as just numbers on a screen that can be traded. Viewing shares this way requires neither rigorous analysis nor knowledge of the underlying business – moreover, trading in and on itself can be exciting and, if the market is rising, lucrative. But essentially it is, in my opinion, still speculating, not investing. There may be a buyer at a higher price – a greater fool – or there may not.

December 2021